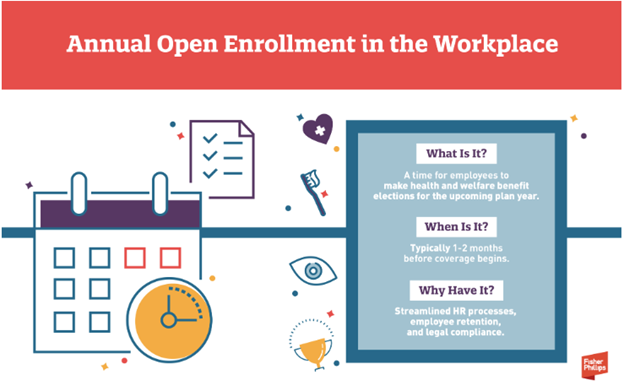

Open enrollment season is upon us, so employers are preparing to provide health and welfare benefit options for their employees during the upcoming plan year. This is an opportunity to ensure compliance with legal requirements. Here are five important considerations employers should keep in mind during open enrollment along with practical ways to help you stay on track. Please keep in mind that this is not intended to be considered legal, financial, or medical advice.

- Employer Mandate Under the Affordable Care Act (ACA)

The Affordable Care Act (ACA) requires Applicable Large Employers (ALEs) to offer health insurance coverage to full-time employees and their dependents. If an ALE fails to do this, they risk facing penalties from the Internal Revenue Service (IRS). During open enrollment, it is crucial to give employees an “effective opportunity” to enroll or decline coverage for the upcoming year.

An “effective opportunity” means providing adequate notice of coverage options, reasonable time for employees to decide, and clear terms on the offer. For ALEs, offering automatic rollover of coverage from the prior year is acceptable, but open enrollment still plays a key role in allowing employees to review and change their elections. UniqueHR clients and their employees must review and re-elect their benefits options annually, as we do not offer automatic rollover of coverage.

Employer Takeaway: If you are an ALE, ensure that all full-time employees and their dependents are given a chance to make coverage elections for the new year. Even if you are not an ALE, check whether your insurance carrier or contractual agreements require a specific open enrollment period.

- Cafeteria Plans Under the Internal Revenue Code (IRC)

Cafeteria plans allow employees to pay for benefits like health insurance premiums with pre-tax dollars, making them a popular option. However, under IRC Section 125, these elections must be made before the plan year begins and typically cannot be changed mid-year, except under limited circumstances.

Open enrollment is the time when employees need to make these pre-tax elections. Employers should ensure that the election process is clear, whether through affirmative elections, default options, or rollover plans (when applicable) from the previous year.

Employer Takeaway: Review your cafeteria plan’s election process to ensure compliance with tax rules. Give employees enough time to make elections before the new plan year and clearly explain the process and any rules regarding election changes.

- IRS Limits for Account-Based Plans

Some employers offer account-based plans, such as Health Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs), which allow employees to set aside pre-tax dollars for qualifying medical expenses. The IRS sets annual limits for these accounts, and it is important to ensure your benefits are in line with these limits.

Here are the contribution limits established by the IRS for 2025:

Health Savings Account:

- Individual Coverage: The contribution limit is $4,300, up from $4,150 in 2024.

- Family Coverage: The contribution limit is $8,850, up from $8,300 in 2024.

- Catch-Up Contributions: (age 55 or older): The limit remains $1,000.

Flexible Savings Account:

- Healthcare FSA: The contribution limit is $3,300, up from $3,050 in 2024.

- Dependent Care FSA: The contribution limit remains at $5,000 (or $2,500 if married and filing separately).

Health Reimbursement Account:

- Expected Benefit HRA (EBHRA): The maximum contribution is $2,150

Employer Takeaway: During open enrollment, confirm that your plan materials reflect the correct IRS limits and communicate clearly whether unused funds can be carried over or are subject to a “use-it-or-lose-it” rule.

- COBRA and FMLA Considerations

Employers must also consider the rights of employees on COBRA or Family and Medical Leave Act (FMLA) leave during open enrollment. COBRA generally requires offering the same benefits to qualified beneficiaries as are available to active employees. This means that individuals on COBRA continuation coverage must be given the same opportunity to make benefit elections as any other employee during open enrollment.

Employees on FMLA leave should be treated as active employees during the open enrollment process. They must be given the opportunity to make benefit elections, including adding or eliminating coverage for dependents.

Employer Takeaway: Ensure that your open enrollment process includes any COBRA beneficiaries and employees on FMLA leave, offering them the same options as active employees.

- Required Disclosures Under ERISA and Other Laws

The Employee Retirement Income Security Act (ERISA) and other laws, such as COBRA and the ACA, require employers to provide certain disclosures to employees during open enrollment. These disclosures include a Summary of Benefits and Coverage (SBC) and other legally required notices about the available health plans.

Employers should make sure that all required documents are provided to eligible employees during open enrollment. Failing to do so could lead to penalties and compliance issues.

Employer Takeaway: Review the disclosure requirements under ERISA, COBRA, and other applicable laws, and ensure that all necessary documents are ready for distribution during open enrollment. It is a good idea to work with your insurance carriers to ensure timely delivery of these materials.

In Conclusion

Navigating open enrollment season is not just about offering benefits; it is about ensuring compliance with various legal requirements. By understanding the considerations outlined above you can streamline the process while minimizing legal risks. Proper planning and communication during open enrollment will help protect your company and ensure a smooth experience for your employees.